Attorney-Approved Promissory Note Template

In the world of lending and borrowing, the importance of a clear, binding agreement cannot be overstated. Enter the promissory note, a financial instrument that plays a pivotal role in detailing the terms under which money has been lent and the commitment of the borrower to pay back the specified sum under agreed conditions. This document is more than just a piece of paper; it's a legally enforceable agreement that spells out the amount of money borrowed, the interest rate if any, the repayment schedule, and what happens in the event of a default. It offers a sense of security to the lender and a clear set of obligations to the borrower. Whether it's issued by individuals in a private loan agreement, or by entities in a more formal lending situation, the promissory note serves as a critical component in financial transactions, ensuring both parties are on the same page and reducing potential disputes. The versatility of a promissory note means it can be tailored to suit a wide range of borrowing and lending scenarios, making it an indispensable tool in the financial toolkit.

Promissory NoteTemplates for Specific US States

Promissory Note Types

Promissory Note Preview

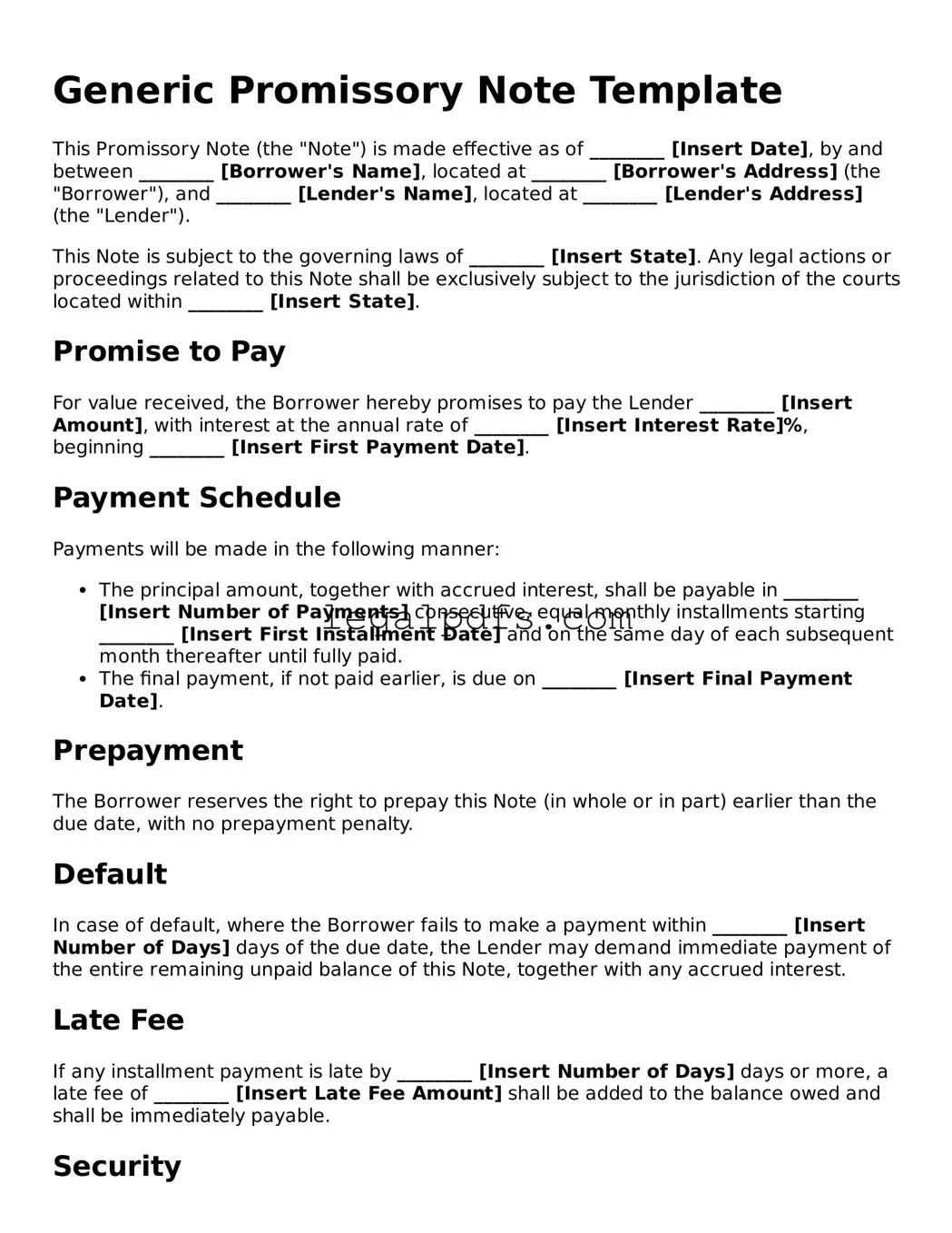

Generic Promissory Note Template

This Promissory Note (the "Note") is made effective as of ________ [Insert Date], by and between ________ [Borrower's Name], located at ________ [Borrower's Address] (the "Borrower"), and ________ [Lender's Name], located at ________ [Lender's Address] (the "Lender").

This Note is subject to the governing laws of ________ [Insert State]. Any legal actions or proceedings related to this Note shall be exclusively subject to the jurisdiction of the courts located within ________ [Insert State].

Promise to Pay

For value received, the Borrower hereby promises to pay the Lender ________ [Insert Amount], with interest at the annual rate of ________ [Insert Interest Rate]%, beginning ________ [Insert First Payment Date].

Payment Schedule

Payments will be made in the following manner:

- The principal amount, together with accrued interest, shall be payable in ________ [Insert Number of Payments] consecutive, equal monthly installments starting ________ [Insert First Installment Date] and on the same day of each subsequent month thereafter until fully paid.

- The final payment, if not paid earlier, is due on ________ [Insert Final Payment Date].

Prepayment

The Borrower reserves the right to prepay this Note (in whole or in part) earlier than the due date, with no prepayment penalty.

Default

In case of default, where the Borrower fails to make a payment within ________ [Insert Number of Days] days of the due date, the Lender may demand immediate payment of the entire remaining unpaid balance of this Note, together with any accrued interest.

Late Fee

If any installment payment is late by ________ [Insert Number of Days] days or more, a late fee of ________ [Insert Late Fee Amount] shall be added to the balance owed and shall be immediately payable.

Security

This Note is / is not secured by collateral. If this Note is secured, the collateral is described as follows: ________ [Describe Collateral].

Governing Law

This Note shall be governed by and construed in accordance with the laws of the State of ________ [Insert State], without regard to its conflict of laws principles.

Amendments

This Note may only be amended or modified by a written agreement signed by both the Borrower and the Lender.

Signatures

This Note is not valid until signed by both parties. The Borrower and Lender signify their agreement with this Note by their signatures below:

Borrower's Signature: ________

Date: ________

Lender's Signature: ________

Date: ________

Document Characteristics

| Fact Number | Fact Detail |

|---|---|

| 1 | A promissory note is a written promise to pay a specific sum of money to a specific person at a specified time or on demand. |

| 2 | It includes the principal amount, interest rate, maturity date, and the signatures of the parties involved. |

| 3 | The person promising to pay is known as the maker or issuer, while the person entitled to receive payment is the payee. |

| 4 | Interest rates on a promissory note can be fixed or variable, directly impacting the total amount to be repaid. |

| 5 | Promissory notes can be secured or unsecured. Secured notes are backed by collateral, whereas unsecured notes are not. |

| 6 | They are used in various financial and real estate transactions, including personal loans, business loans, and student loans. |

| 7 | State laws govern the creation and enforcement of promissory notes, and these laws can vary significantly from one state to another. |

| 8 | In the event of a default, the holder of a promissory note may take legal action to recover the debt. |

| 9 | A promissory note must be dated, and both parties should retain a copy for their records. |

| 10 | For real estate transactions, promissory notes are often accompanied by a mortgage or deed of trust as security for the loan. |

Promissory Note: Usage Instruction

When preparing to fill out a Promissory Note form, it's crucial to proceed with attention to detail and clear understanding. This document serves as a formal agreement between two parties: the one who is borrowing money and the one who is lending it. The completed form will outline the repayment schedule, the interest rate, if applicable, and any other terms related to the loan. Ensuring accuracy in this process is essential as it legally binds both parties to the agreed-upon terms. Follow the steps below to complete the form accurately.

- Enter the Date: At the top of the form, specify the date on which the promissory note is made. This should include the day, month, and year.

- Identify the Parties: Clearly write the full legal names of both the borrower and the lender. Include addresses and contact information if required by the form.

- Loan Amount: Specify the total amount of money being borrowed. Make sure to write this amount in both words and numbers to avoid any confusion.

- Interest Rate: If applicable, record the annual interest rate that the borrower agrees to pay. This should be a percentage of the principal loan amount.

- Repayment Schedule: Detail the terms of repayment. This might include the total number of payments, the frequency of payments (monthly, quarterly, etc.), and when the first payment is due. Be clear about the final due date for the loan to be fully repaid.

- Collateral: If the loan is secured with collateral, describe the property or asset being used as security. Include any pertinent details that clearly identify the collateral.

- Late Fees and Penalties: Describe any late fees or penalties for missed or late payments. Specify the grace period before a payment is considered late and the exact fee or rate of the penalty.

- Signatures: Both the borrower and the lender must sign and date the form. Witness signatures may also be required depending on the legal requirements of the jurisdiction.

Once the form is accurately completed and signed, it should be kept in a safe but accessible place. Both the borrower and the lender should have copies for their records. This document will serve as a vital reference throughout the term of the loan, ensuring that both parties adhere to their agreed commitments. Executing this form with care establishes a clear understanding and helps to prevent any potential disputes in the future.

Obtain Clarifications on Promissory Note

What is a Promissory Note?

A Promissory Note is a legal document that outlines a promise made by one party, the borrower, to pay back a specified sum of money to another, the lender. This document serves as a formal declaration of the borrower's commitment to repay the loan under defined terms, including the loan amount, interest rate, repayment schedule, and any other conditions agreed upon by both parties.

Why is a Promissory Note important?

Having a Promissory Note is crucial as it legally binds the borrower to repay the borrowed amount, which provides security for the lender. It also clearly documents the loan's terms, helping to prevent misunderstandings and disputes over the repayment terms. In the event of non-payment, the note provides the lender with a legal pathway to seek recovery of the funds.

What are the key components of a Promissory Note?

Key components of a Promissory Note include the amount borrowed, interest rate, repayment schedule (dates and amounts), information about the parties involved (borrower and lender), signatures of both parties, and the date of the agreement. Optional clauses may include penalties for late payments, a provision for acceleration of the debt, and security/collateral backing the loan.

Is a Promissory Note legally binding?

Yes, a Promissory Note is a legally binding document. Once signed by both the borrower and the lender, it obligates the borrower to repay the loan according to the terms laid out in the agreement. Failure to comply with these terms can result in legal repercussions for the borrower, including lawsuits and damage to their credit rating.

Can a Promissory Note include collateral?

Absolutely. A Secured Promissory Note includes a clause that ties the repayment of the loan to a piece of collateral, usually property or a valuable asset. If the borrower fails to repay the loan, the lender has the right to seize the collateral as repayment for the debt. This provides an extra layer of security for the lender.

What happens if a borrower does not repay a Promissory Note?

Should a borrower fail to repay the loan as agreed, the lender has the right to take legal action to recover the debt. This can include filing a lawsuit against the borrower, seizing collateral if the note is secured, and pursuing other legal avenues to ensure repayment. It's important for borrowers to communicate with lenders if they're unable to meet repayment commitments to potentially negotiate alternative arrangements.

Can the terms of a Promissory Note be modified?

Yes, the terms of a Promissory Note can be modified, but any modifications must be agreed upon by both the borrower and the lender. The changes should be documented in writing, and both parties should sign any addendum or modification document. This ensures that the updated terms are enforceable and clear to both sides.

Do Promissory Notes need to be notarized?

While notarization is not always a legal requirement for Promissory Notes, getting the document notarized can add an extra layer of legal protection. Notarization formally verifies the identity of the parties signing the document, which can be helpful in preventing disputes over the validity of signatures or the terms of the loan.

How can a Promissory Note be enforced?

To enforce a Promissory Note, the lender may need to take legal action against the borrower if they fail to repay according to the terms. This can involve filing a lawsuit for breach of contract. The specific enforcement methods available will depend on the terms of the note and the laws of the jurisdiction where it was issued. For secured loans, the process may include seizing and selling the collateral. It is advisable for lenders to consult with legal professionals to explore their options.

Common mistakes

Filling out a Promissory Note, an important document that outlines the details of a loan between two parties, can often be a straightforward process. However, it's easy to make mistakes that can lead to big problems down the line. First and foremost, many people fail to specify the terms of repayment in clear, understandable language. This includes not only the repayment amount but also the schedule and any interest rates applied. Without these critical details being clearly outlined, misunderstandings can arise, leaving either party at a disadvantage.

Another common error is neglecting to include the legal names of all parties involved. Sometimes, individuals might use nicknames or incomplete names, but for a Promissory Note to hold legal weight, full legal names must be used. This ensures that the document is enforceable in a court of law, should any disputes arise. Without the correct names, the credibility and enforceability of the note can be severely compromised.

Overlooking the necessity of having the note witnessed or notarized is another oversight some people make. While not all states require a Promissory Note to be notarized, having an impartial third party witness the signing of the document can add an extra layer of legal protection. This can be particularly crucial if the agreement goes south and one party needs to prove the validity of the document in court.

Last but not least, failing to keep a copy of the Promissory Note is a mistake that can easily be avoided. Both the borrower and the lender should keep a signed copy of the note. This serves as a physical record of the agreement and can be invaluable in the event of a dispute or if there is a need to reference the terms of the loan at a later date. In the digital age, electronic copies can also serve this purpose, provided they are stored securely.

Documents used along the form

When entering into an agreement that involves lending or borrowing money, a Promissory Note is a crucial document. It outlines the terms under which money is loaned and the repayment schedule. However, to ensure the transaction is comprehensively documented and both parties are protected, several other forms and documents are typically used in conjunction with a Promissory Note. These documents serve various purposes, from securing the loan to detailing the consequences of non-payment.

- Loan Agreement: A more detailed contract than a Promissory Note, which includes the obligations and responsibilities of each party, interest rates, repayment plans, and the consequences of late payments or default.

- Security Agreement: This document is used when the loan is secured with collateral. It details the assets pledged by the borrower to secure the loan, ensuring the lender has a claim to the collateral if the borrower defaults.

- Guaranty: A legal commitment by a third party to repay the loan if the borrower fails to do so. This adds an additional layer of protection for the lender.

- Mortgage or Deed of Trust: For loans secured by real estate, this document places a lien on the property as collateral for the loan. It details the rights and obligations of both parties regarding the property.

- Amortization Schedule: An itemized list of payments for the loan term, showing how each payment is divided into principal and interest. It helps both parties track the progress of loan repayment.

- Default Notice: A formal notice issued by the lender to the borrower in the event of a missed payment or other violation of the loan terms. It specifies the breach and the actions required to remedy it.

Together, these documents form a robust framework that supports the original Promissory Note. They ensure clarity and mutual understanding, help manage expectations, and provide mechanisms for dealing with various situations that might arise during the life of the loan. By thoroughly documenting the loan process, both lenders and borrowers can protect their interests and foster a positive financial relationship.

Similar forms

Loan Agreement: Just like a promissory note, a loan agreement is a legally binding document between a lender and a borrower. However, it is more comprehensive, detailing the repayment schedule, interest rates, and what happens in case of default.

Mortgage Note: This is a form of promissory note specifically tied to real estate transactions. It outlines the loan details for the purchase of property, but it is secured against the property being bought. If payments aren't made, the lender can foreclose on the property.

IOU (I Owe You): An IOU is a simpler, informal acknowledgment of debt, similar to a promissory note. However, it lacks the detailed repayment terms and legal protections typically found in a promissory note.

Personal Guarantee: While not a loan document, a personal guarantee is related in that it involves a promise to pay. It's an individual's legal promise to repay credit issued to a business for which they serve as an executive or partner, similar to how a promissory note is a commitment to repay a loan.

Bill of Sale: A bill of sale is another document that signifies an agreement between two parties. It's mainly used in the sale of personal property (e.g., vehicles) and serves as proof of transfer of ownership. Unlike a promissory note, it doesn't detail repayment terms but similarly formalizes an agreement.

Lease Agreement: Similar to promissory notes in its function as a binding agreement, a lease agreement outlines terms between a landlord and tenant, including payment. However, it pertains to the rental of property rather than the borrowing of money.

Credit Agreement: This document outlines the terms under which credit is extended to a borrower. Like a promissory note, it includes repayment terms and interest rates but is typically more detailed and involves larger sums of money or credit.

Bond Instrument: Bonds are investment instruments representing a loan made by an investor to a borrower, often corporate or governmental. They share similarities with promissory notes in terms of being written promises to pay back a principal along with interest. Yet, bonds are traded in financial markets, which doesn’t typically happen with promissory notes.

Dos and Don'ts

When filling out the Promissory Note form, it is essential to follow specific guidelines to ensure accuracy and legality. Below are lists of what you should do and what you shouldn't do during this process.

Do:

- Verify the accuracy of all names and addresses of both the lender and borrower. It is crucial to ensure these details are correct to avoid any future disputes or confusion.

- Clearly state the loan amount in both numbers and words to prevent any misunderstandings about the total sum being borrowed.

- Include a detailed repayment schedule. Outlining the frequency of payments and due dates helps both parties understand the expectations and avoid missed payments.

- Specify the interest rate if applicable. This should be done clearly to avoid ambiguity and ensure compliance with state laws.

- Sign and date the form in front of a notary. This step adds a level of formality and authenticity to the document, making it legally binding.

- Keep a copy of the signed promissory note for personal records. Having proof of the agreement is essential for both the borrower and the lender.

Don't:

- Leave any fields blank. Incomplete forms can lead to misunderstandings or potential legal issues in the future.

- Sign the document without thoroughly reading and understanding every section. This helps prevent agreeing to terms that could be unfavorable.

- Use unclear or vague language. Precision in wording prevents disputes over the interpretation of the terms.

- Forget to specify whether the loan is secured or unsecured. This detail can significantly affect the agreement's terms and enforcement.

- Ignore state laws regarding loan agreements. Compliance with local regulations is crucial to ensure the note's enforceability.

- Omit details about any agreed-upon late fees or penalties for missed payments. Including this information upfront can save both parties from future conflicts.

Misconceptions

Promissory notes are widely used documents that outline how a borrower promises to repay a lender according to the terms they've agreed upon. However, there are several misconceptions about promissory notes that need clarification:

Only financial institutions can issue them. People often think that promissory notes can only be issued by banks or financial institutions. In reality, any individual or business entity can issue a promissory note as long as the involved parties agree on the repayment terms.

They must follow a standard format. While it's true that certain information must be included for a promissory note to be considered valid (such as the amount borrowed, interest rate, and repayment schedule), there isn't a mandatory format. The parties can customize the document to suit their agreement.

Signing a promissory note means you have accepted the loan terms. This misconception can lead to confusion. Signing a promissory note is indeed an acceptance of the loan's terms, but it's crucial for both lender and borrower to fully understand and agree upon these terms before signing.

They are legally binding in any form. While promissory notes are legal documents, they must contain specific elements to be enforceable in court, such as the signature of the borrower. A note missing key elements may not be legally binding.

Interest rates on promissory notes are optional. Some believe that interest rates are not a mandatory component of a promissory note. However, including an interest rate is standard practice and can affect the legality of the note, especially in cases where not charging interest could be considered a gift.

All promissory notes are the same. There are several types of promissory notes, including secured, unsecured, simple, and demand notes. Each serves different purposes and comes with its own set of terms and conditions.

A verbal agreement is as good as a written promissory note. While verbal agreements can be legally binding, a written promissory note provides a clear, enforceable record of the loan's terms. Relying solely on a verbal agreement can lead to disputes and challenges in proving the agreement's specifics.

Key takeaways

When dealing with the Promissory Note form, it's essential to approach the document with attention to detail and full awareness of its legal importance. This form not only signifies a promise to repay a loan but also outlines the terms and conditions of such repayment. Understanding its components can protect both the lender and borrower from future disputes. Below are key takeaways for properly filling out and using a Promissory Note form.

- Personal Information: Ensure that the names and addresses of both the borrower and lender are completely and correctly detailed. This information establishes the parties to the agreement and facilitates future communication.

- Loan Amount: Clearly state the exact amount of money being loaned. This figure should include the principal amount without any interest.

- Interest Rate: Specify the interest rate agreed upon. This rate should be clear, specifying if it's annual or for the duration of the loan, to prevent any confusion regarding additional charges.

- Repayment Terms: Clearly outline how the loan will be repaid. This includes the schedule (monthly, quarterly, yearly), the amount of each payment, and over what period. These details are crucial to both parties understanding their obligations.

- Secured or Unsecured: Indicate whether the loan is secured (backed by collateral) or unsecured. If secured, explicitly describe the collateral in detail to avoid ambiguity.

- Co-signer Information: If a co-signer is part of the agreement, their information should be included, similar to the main parties. This inclusion further guarantees the loan's repayment.

- Default Terms: Define what constitutes a default on the loan and the subsequent steps or remedies. These terms offer protection to the lender while giving fair warning to the borrower.

- Governing Law: Specify which state law will govern the Promissory Note. Laws vary from state to state, and choosing a governing law clarifies which state's regulations apply to the agreement.

- Signatures: Ensure that all parties, including co-signers if applicable, sign the note. Signatures legally bind the parties to the agreement's terms and acknowledge their understanding and consent.

- Witnesses or Notarization: Depending on the laws of the governing state or the complexity of the loan, having the signatures witnessed or the document notarized can add an additional layer of legal protection and authenticity.

Thoroughly reviewing the Promissory Note form before finalizing can prevent misunderstandings and potential legal complications down the road. Both the lender and the borrower should keep a copy of the signed document for their records, ensuring that both have access to the agreed-upon terms.

Check out Other Templates

Single Certificate - For those separated but not legally divorced, obtaining and accurately completing this affidavit can be more complex and might require legal guidance.

Bill of Sale Creator - It is a straightforward way to ensure that all necessary information is recorded and agreed upon by both parties.