Attorney-Approved Vehicle Repayment Agreement Template

When individuals decide to purchase a vehicle through financing or when they need to restructure an existing auto loan due to financial difficulties, a Vehicle Repayment Agreement form becomes a crucial document. This form, essentially a contract between the borrower and the lender, outlines the terms of repayment, including loan amounts, interest rates, payment schedules, and consequences of default. It serves as a legal record ensuring that both parties have a mutual understanding of the financial arrangement. Furthermore, the agreement is designed to protect the interests of both the lender, by providing a mechanism to recover the loaned amount, and the borrower, by stipulating clear, manageable terms for repayment. In scenarios where misunderstandings or disputes arise, the Vehicle Repayment Agreement can be a vital reference that helps resolve issues by referring back to the agreed-upon terms. For these reasons, it is imperative for both lenders and borrowers to thoroughly understand the details of the agreement before signing. This document not only facilitates a smoother financial transaction but also serves as a safeguard against potential legal disputes, making it an indispensable part of financing or refinancing a vehicle.

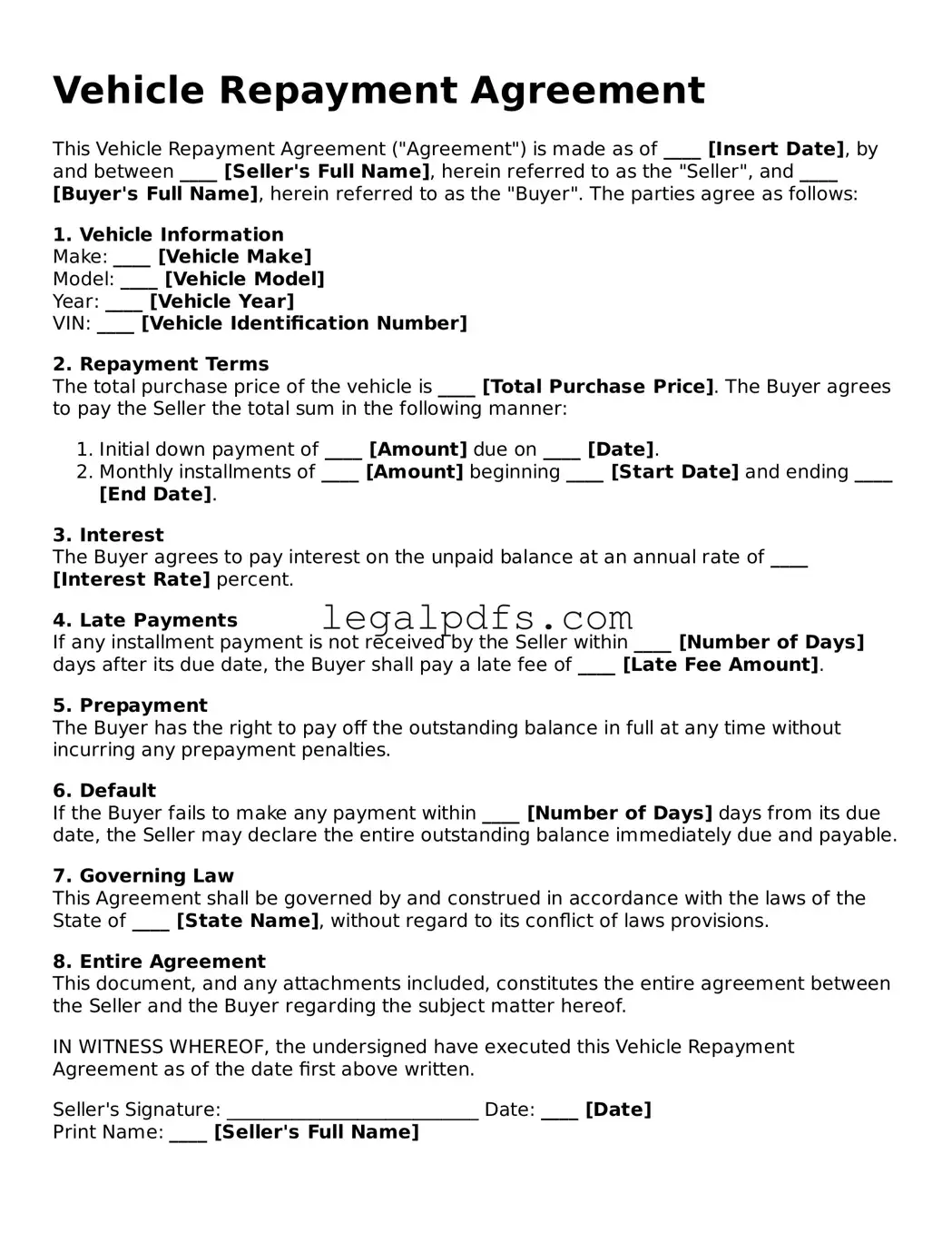

Vehicle Repayment Agreement Preview

Vehicle Repayment Agreement

This Vehicle Repayment Agreement ("Agreement") is made as of ____ [Insert Date], by and between ____ [Seller's Full Name], herein referred to as the "Seller", and ____ [Buyer's Full Name], herein referred to as the "Buyer". The parties agree as follows:

1. Vehicle Information

Make: ____ [Vehicle Make]

Model: ____ [Vehicle Model]

Year: ____ [Vehicle Year]

VIN: ____ [Vehicle Identification Number]

2. Repayment Terms

The total purchase price of the vehicle is ____ [Total Purchase Price]. The Buyer agrees to pay the Seller the total sum in the following manner:

- Initial down payment of ____ [Amount] due on ____ [Date].

- Monthly installments of ____ [Amount] beginning ____ [Start Date] and ending ____ [End Date].

3. Interest

The Buyer agrees to pay interest on the unpaid balance at an annual rate of ____ [Interest Rate] percent.

4. Late Payments

If any installment payment is not received by the Seller within ____ [Number of Days] days after its due date, the Buyer shall pay a late fee of ____ [Late Fee Amount].

5. Prepayment

The Buyer has the right to pay off the outstanding balance in full at any time without incurring any prepayment penalties.

6. Default

If the Buyer fails to make any payment within ____ [Number of Days] days from its due date, the Seller may declare the entire outstanding balance immediately due and payable.

7. Governing Law

This Agreement shall be governed by and construed in accordance with the laws of the State of ____ [State Name], without regard to its conflict of laws provisions.

8. Entire Agreement

This document, and any attachments included, constitutes the entire agreement between the Seller and the Buyer regarding the subject matter hereof.

IN WITNESS WHEREOF, the undersigned have executed this Vehicle Repayment Agreement as of the date first above written.

Seller's Signature: ___________________________ Date: ____ [Date]

Print Name: ____ [Seller's Full Name]

Buyer's Signature: ___________________________ Date: ____ [Date]

Print Name: ____ [Buyer's Full Name]

Document Characteristics

| Fact Name | Description |

|---|---|

| Purpose | The Vehicle Repayment Agreement form is designed to help parties structure the terms under which a vehicle will be paid off, covering both the payment schedule and any interest to be applied. |

| Applicability | This form is relevant for buyers and sellers entering into a private vehicle sale, where the buyer will not be paying the full price upfront and thus requires a structured payment plan. |

| Content Requirement | The agreement typically includes details such as the total sale price, payment increments, timeline for payment completion, interest rate (if applicable), and consequences of default. |

| Governing Law | For state-specific Vehicle Repayment Agreements, the governing laws are those of the state in which the agreement is made and will define how the agreement is interpreted and enforced. |

| Signing Requirement | Both the buyer and the seller need to sign the agreement, often in the presence of a notary, to validate the agreement legally and ensure the acknowledgment of the terms by both parties. |

Vehicle Repayment Agreement: Usage Instruction

When embarking on the task of filling out a Vehicle Repayment Agreement form, it's essential to proceed with accuracy and attention to detail. This document is crucial for establishing a clear and legally binding agreement between the creditor and debtor, regarding the repayment of a vehicle loan. The steps outlined below have been designed to guide individuals through the process of completing this form accurately, ensuring that all pertinent information is documented. Following these steps will not only streamline the process but will also help in preventing future disputes or misunderstandings related to the repayment terms of the vehicle loan.

- Begin by filling out the date at the top of the form. This should be the current date on which the agreement is being made.

- Enter the full legal names and contact information of both the creditor (the individual or entity providing the loan) and the debtor (the individual or entity receiving the loan and purchasing the vehicle).

- Provide a detailed description of the vehicle being purchased. This should include the make, model, year, color, VIN (Vehicle Identification Number), and any other identifying details.

- Clearly state the total loan amount being borrowed for the purchase of the vehicle. Be sure to include the currency.

- Document the agreed-upon repayment schedule. This should include the frequency of payments (e.g., monthly), the amount of each payment, the due date for the first payment, and the due date for the final payment.

- Specify the interest rate, if applicable, that will be applied to the loan amount. This should be expressed as an annual percentage rate (APR).

- Detail any penalties or fees for late payments or defaulting on the loan. This section should outline the consequences of failing to adhere to the agreed-upon repayment schedule.

- Include a clause about the security interest, stating that the creditor will hold a security interest in the vehicle until the loan is fully repaid. This means the vehicle serves as collateral for the loan.

- Both the creditor and debtor must sign and date the form, acknowledging their understanding and agreement to the terms outlined. It is recommended to have a witness sign as well, although this may not be required in all jurisdictions.

- Lastly, ensure that all blanks are filled in and no sections have been inadvertently skipped. Review the form for any errors or omissions before finalizing the document.

Following the completion of the Vehicle Repayment Agreement form, it should be executed according to the laws and regulations of the jurisdiction in which it is being used. This often includes having the document notarized, although requirements can vary. Both parties should retain copies of the signed agreement for their records. Doing so ensures that both the creditor and debtor have a tangible record of their commitments, potentially alleviating future conflicts related to the vehicle's repayment terms.

Obtain Clarifications on Vehicle Repayment Agreement

What is a Vehicle Repayment Agreement?

A Vehicle Repayment Agreement is a legal contract between the seller of a vehicle and the buyer, which outlines the terms and conditions under which the buyer agrees to pay back the purchase price of the vehicle to the seller. This agreement typically includes details such as the total amount to be repaid, the schedule of payments, interest rates, and the consequences of failing to make payments as agreed.

Who needs to sign the Vehicle Repayment Agreement?

Both the seller of the vehicle and the buyer must sign the Vehicle Repayment Agreement. Their signatures legally bind them to the terms and conditions outlined in the document. In some cases, a witness or a legal representative may also be required to sign the agreement, depending on the laws of the jurisdiction where the agreement is executed.

Does the Vehicle Repayment Agreement need to be notarized?

Whether a Vehicle Repayment Agreement needs to be notarized can vary based on local and state laws. In many jurisdictions, notarization is not mandatory, but it can add a level of legal authenticity and help prevent disputes over the validity of the agreement. It's advisable to check the specific requirements in your area.

What happens if payments are not made as agreed?

If payments are not made according to the agreed-upon schedule, the seller has the right to take legal actions based on the terms specified in the Vehicle Repayment Agreement. This could include reclaiming possession of the vehicle, reporting the default to credit bureaus, or initiating a legal process to recover the owed amount. The exact consequences depend on the agreement's terms and applicable laws.

Can the payment terms be modified after the agreement is signed?

Payment terms can be modified after signing the agreement, but any changes need the consent of both the seller and the buyer. It's best to document any agreed modifications in a written amendment to the original agreement to avoid future disputes.

Is a down payment required for a Vehicle Repayment Agreement?

While a down payment is not legally required for a Vehicle Repayment Agreement, sellers often require one. A down payment can reduce the total amount financed, potentially lower the interest rate, and provide security to the seller. The requirement and amount of a down payment should be clearly specified in the agreement.

How is interest calculated in a Vehicle Repayment Agreement?

Interest in a Vehicle Repayment Agreement is typically calculated based on an annual percentage rate (APR). The method of calculation—whether simple or compound interest—should be specified in the agreement. The total interest amount reflects the cost of borrowing over the term of the loan and is influenced by the loan amount, interest rate, and payment schedule.

What personal information is needed for a Vehicle Repayment Agreement?

The agreement must include personal information for both the buyer and the seller, such as full names, addresses, and contact information. It may also require details about the vehicle, including make, model, year, VIN (Vehicle Identification Number), and current mileage, to accurately identify the subject of the agreement.

Can the Vehicle Repayment Agreement be terminated early?

Early termination of the agreement is subject to the terms laid out in the document. In many cases, early payoff may be allowed, potentially including a penalty or the waiving of remaining interest. However, specific provisions for early termination should be clearly outlined in the agreement to avoid misunderstandings.

What safeguards does a Vehicle Repayment Agreement provide?

A Vehicle Repayment Agreement provides legal protection and clarity for both the buyer and the seller. For the seller, it ensures a structured repayment plan and recourse in case of non-payment. For the buyer, it lays out the financial obligations for obtaining the vehicle and can protect against unfair practices. It serves to prevent disputes by specifying the terms of the deal in detail.

Common mistakes

Filling out a Vehicle Repayment Agreement form can seem straightforward, but errors can lead to significant complications down the road. A common mistake is neglecting to thoroughly review the document for accuracy. Individuals often rush through filling out forms, overlooking critical details such as the correct spelling of names, addresses, and the accurate figures for the loan amounts and interest rates. This can lead to misunderstandings or legal issues if the agreement needs to be enforced.

Another frequent oversight is the failure to specify the repayment schedule in clear terms. This part of the agreement outlines when payments are due, the amount of each payment, and where payments should be sent. Without clear terms, there can be disputes over missed or late payments, potentially leading to unnecessary conflict between the parties involved.

Some people also make the mistake of not including clear terms regarding late fees or missed payments. This oversight can result in ambiguity about the consequences if a payment is not made on time. It is crucial to specify any additional fees or interest that will accrue on late payments to ensure both parties are fully informed.

Forgetting to detail the vehicle's condition and specifications is another common error. The agreement should include the make, model, year, mileage, and VIN (Vehicle Identification Number) to avoid any confusion about the vehicle being sold or used as collateral. This is particularly important in distinguishing the specified vehicle from others that might be similar.

Not delineating the warranty or "as is" status of the vehicle is a mistake that can lead to future disputes. It's vital to clearly state whether the vehicle comes with a warranty and the terms of that warranty, or if it is being sold "as is," meaning the buyer accepts the vehicle with all its current faults and issues.

Another error involves ignoring state-specific requirements or not including required legal phrases. Each state may have different laws regarding vehicle repayment agreements, and failing to comply with these laws can render the agreement invalid or unenforceable. It's important to research and include any state-specific terms or disclosures.

Finally, not having the agreement signed by all parties involved, or failing to get proper witness or notarization where required, is a critical mistake. Signatures validate the agreement, making it legally binding, and the absence of required witness or notarization signatures can compromise the document's enforceability. Always check to see if your state requires witness or notarization for this type of agreement.

Documents used along the form

When entering into a Vehicle Repayment Agreement, several other forms and documents are often instrumental to ensure clarity, legality, and the comprehensive nature of the financial arrangement. These documents help in detailing the specifics of the agreement, protecting the interests of the involved parties, and providing legal evidence if disputes arise. Here is a list of some of these critical documents.

- Bill of Sale: This document acts as a receipt for the purchase, detailing the final price agreed upon for the vehicle, the date of sale, and the parties involved. It serves as proof of transfer of ownership.

- Promissory Note: Often accompanying a Vehicle Repayment Agreement, a promissory note outlines the borrower’s promise to repay the loan. It specifies the loan amount, interest rate, repayment schedule, and any penalties for late payments.

- Loan Amortization Schedule: This document provides a detailed schedule of payments over the loan term, showing how each payment is split between the principal amount and interest, and how the balance reduces over time.

- Vehicle Title: The vehicle title is a critical document that proves ownership. When a vehicle is under a repayment plan, lenders may hold onto the title until the loan is fully repaid.

- Insurance Proof: Lenders often require proof of insurance to ensure the vehicle is covered against accidents, theft, and other damages during the loan period.

- Vehicle Service Records: Comprehensive service records can assure a lender of the vehicle's upkeep and condition, potentially influencing the loan terms.

- Government Issued Identification: Most financial transactions require identification to verify the identities of the parties involved. This could include a driver’s license or passport.

This ensemble of documents complements the Vehicle Repayment Agreement by providing a framework that safeguards the transaction. Each document fills a unique role, ensuring that the agreement adheres to legal standards and that both lender and borrower responsibilities are clear and enforceable. These tools collectively facilitate a smoother transaction, minimize potential misunderstandings, and provide a pathway for legal recourse if the need arises.

Similar forms

Loan Agreement: Similar to a Vehicle Repayment Agreement, a Loan Agreement outlines the terms under which money is lent to a borrower. Both documents specify the amount to be repaid, the repayment schedule, and the interest rates, ensuring that both parties are clear on their obligations and rights.

Lease Agreement: This contract involves renting an asset and is similar to a Vehicle Repayment Agreement in that it details payment terms, such as monthly amounts and due dates. While a Lease Agreement typically involves renting property or equipment, both agreements establish the responsibilities of each party for the duration of the agreement.

Promissory Note: A promissory note is a simple document where one party promises to repay a debt to another party under specified terms. Like a Vehicle Repayment Agreement, it defines the loan amount, interest rate, and repayment schedule. However, it's less detailed and usually doesn't include collateral as a Vehicle Repayment Agreement might.

Installment Agreement: An Installment Agreement is used when payments are made in installments over time for the purchase of goods or services. It resembles a Vehicle Repayment Agreement in structure, outlining payment amounts, frequencies, and deadlines, essentially setting the stage for a structured payoff plan.

Mortgage Agreement: While focused on real estate, a Mortgage Agreement shares commonalities with a Vehicle Repayment Agreement by securing a loan with physical property. Both documents specify payment terms, interest rates, and legal implications upon failure to repay, ensuring the lender's investment is protected.

Dos and Don'ts

Filling out the Vehicle Repayment Agreement form requires careful attention to ensure the terms are clear and legally binding. Whether you're the borrower or the lender, here are some dos and don'ts to guide you through the process:

Do:Read the entire form before you start filling it out to understand all the sections and requirements.

Use a pen with black ink for clarity and better photocopying quality.

Ensure all parties involved in the agreement are named accurately with their full legal names.

Be precise with the repayment terms, including the amount, frequency, due dates, and the final payment deadline.

Clarify the interest rate, if applicable, and how it's calculated over the repayment period.

Rush through the process without reviewing each section for completeness and accuracy.

Omit details about the vehicle, such as make, model, year, VIN (Vehicle Identification Number), and current mileage, as this information accurately identifies the vehicle under the agreement.

Forget to specify any penalties for late payments or non-compliance with the terms of the agreement.

Sign the agreement without ensuring that all parties fully understand its terms and conditions.

Remember, a well-documented Vehicle Repayment Agreement can help prevent misunderstandings and legal disputes down the road. It serves as a clear record of the obligations of each party regarding the vehicle payment plan. Always review the final document with all parties involved before signing to ensure the information is correct and agreed upon.

Misconceptions

Many people have misunderstandings about Vehicle Repayment Agreements, which can lead to confusion and possible legal issues. It's important to clarify these misconceptions to ensure both parties enter into the agreement with a clear understanding of their rights and obligations.

- All vehicle repayment agreements are the same.

This is not true. While many vehicle repayment agreements share common elements, such as payment amounts, interest rates, and terms of repayment, the specific details can vary widely based on the lender, the state, and the circumstances of the borrower and seller. Always read the agreement carefully to understand the specifics of your deal.

- You don't need a written agreement if you trust the other party.

Even if you fully trust the person you're dealing with, having a written vehicle repayment agreement is crucial. It provides a clear record of the terms agreed upon and can protect both parties if there's a dispute or misunderstanding in the future.

- Verbal agreements are just as binding as written ones.

Though verbal agreements can be legally binding, proving the terms of a verbal agreement in a dispute can be very challenging. Written agreements are always recommended, especially for complex transactions like vehicle repayments, to ensure all details are documented and enforceable.

- Vehicle repayment agreements don't need to be detailed.

Contrary to this belief, it’s important for a vehicle repayment agreement to be as detailed as possible. This includes specifying payment amounts, dates, interest rates if applicable, consequences of late payments, and what happens in case of default. The more detailed the agreement, the less room there is for misinterpretation.

- You can't modify a vehicle repayment agreement once it's signed.

This isn't necessarily true. Both parties can agree to modify the agreement if needed, but any modifications should be made in writing and signed by both parties. Without this documentation, enforcing changes can be difficult.

- The seller retains ownership of the vehicle until the final payment is made.

This tends to vary based on the agreement and state laws. In some agreements, the buyer might gain ownership of the vehicle immediately and the car serves as collateral for the loan. It's critical to understand how ownership is transferred in your specific agreement to avoid any legal complications.

Key takeaways

When dealing with a Vehicle Repayment Agreement form, it's crucial to navigate through the process with a clear understanding. This agreement is a critical document that outlines the terms between two parties regarding the repayment schedule, interest rate, and other conditions for a loan used to purchase a vehicle. Here are six key takeaways to ensure that the process of filling out and using this form is done correctly and effectively.

- Accuracy is key. Make sure all the information provided in the Vehicle Repayment Agreement is accurate. This includes the full names of the parties involved, the correct vehicle identification number (VIN), and the precise loan amount. Errors can lead to disputes or legal complications down the line.

- Understand the terms. Before signing, both the lender and the borrower should thoroughly understand the terms outlined in the agreement. This includes the repayment schedule, the interest rate, late fees, and what constitutes a default on the loan.

- Keep it legal. Ensure that the agreement complies with state and federal laws. Interest rates and lending practices are regulated, and failure to adhere to these laws can result in penalties or the agreement being declared invalid.

- Notarization may be necessary. Depending on the state, notarizing the agreement might be a requirement to add an extra layer of legality and ensure that the document is enforceable. Check local laws to see if notarization is needed.

- Keep detailed records. Both parties should keep a signed copy of the agreement and any receipts of payments made. This is crucial for maintaining a clear record of the debt repayment and can protect both parties in case of a dispute.

- Amendments should be in writing. If any terms of the agreement need to be changed, the amendments should be made in writing and signed by both parties. Oral agreements or handshake deals can lead to misunderstandings and are more difficult to enforce legally.

By following these guidelines, both lenders and borrowers can ensure that the Vehicle Repayment Agreement form serves its intended purpose and protects the interests of both parties throughout the repayment period.

Check out Other Templates

Bill of Sale Template for Trailer - It's a crucial component of a well-documented transaction, complementing other required documents for trailers such as title and registration.

How Do Wills Work - It provides an avenue for expressing your wishes regarding the continuation or termination of life support in situations where recovery is not expected.